The GoEasy Subprime Warning: How a 57% Stock Crash Signals the Final Stage of the Canadian Housing Bubble

The GoEasy subprime warning of March 2026 represents the most significant credit event in Canada since the 2008 financial crisis. A surprise C$178 million charge-off in its LendCare division triggered a 57% one-day stock plunge on the TSX, signaling that the "debt-service wall" has finally broken for Canada's most vulnerable borrowers. This event acts as a "canary in the coal mine" for the broader housing market, particularly for high-leverage homeowners relying on alternative financing and home equity to bridge the gap during the 2026 mortgage renewal cliff.

I. The Event: A $178 Million Reality Check

On March 10, 2026, GoEasy Ltd. (TSX: GSY) issued a surprise Q4 preview that shattered decades of investor confidence. The company announced a massive C$178 million incremental charge-off, concentrated primarily in its LendCare segment—a merchant-finance arm specializing in auto, powersports, and equipment loans.

This write-down represents approximately 3.2% of its total $5.5 billion loan book in a single stroke. The market reaction was swift and brutal: GSY shares collapsed from ~C$115 to ~C$50, wiping out years of gains and forcing an immediate suspension of dividends.

1.1 The Anatomy of the GoEasy Stock Crash

GoEasy entered 2026 as a darling of the Toronto Stock Exchange, boasting 95 consecutive quarters of profitability. However, earlier in 2025, the company had quietly boosted its allowances for loan losses. Short-seller reports (specifically from Jehoshaphat Research) in late 2025 had already alleged that GoEasy's credit models were over-optimistic. The March 2026 event effectively confirmed those fears, leading to the GoEasy subprime warning that is now echoing through the Canada Housing Crash Risk 2026 analysis.

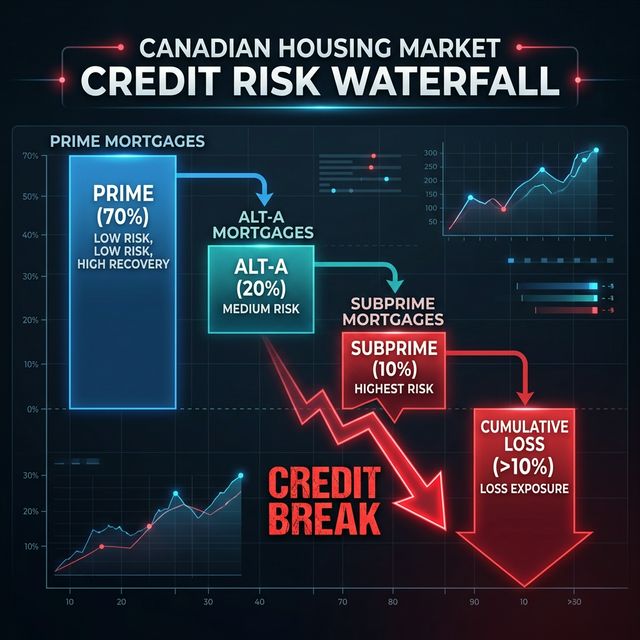

II. Strategic Analysis: The Fatal Flaw in the Subprime Business Model

2.1 easyfinancial: The Home Equity "ATM" for Distressed Borrowers

Much of the growth in easyfinancial came from home equity lines of credit (HELOCs) offered to non-prime borrowers. As traditional banks tightened their stress tests under OSFI rules, thousands of homeowners used easyfinancial to tap into property equity. This "shadow banking" sector has grown to become a crucial component of the Mortgage Renewal Cliff 2026 ecosystem.

2.2 LendCare: The Catalyst for the GoEasy Subprime Warning

Acquired in late 2021 for ~$320M, LendCare was touted as a growth engine. However, the March 2026 crash was driven entirely by LendCare losses. As analyzed by RBC Economics, borrowers faced with the "Mortgage Cliff" prioritized housing over vehicle payments. When a borrower has to choose between their roof and their car, the car is the first to go.

III. The Subprime-Housing Nexus: Why the GoEasy Event is the Final Warning

The GoEasy collapse is not just a fintech story; it is a housing story. The connection lies in how Canadians have managed the 2026 Mortgage Renewal Wave.

3.1 The "Subprime Bridge" is Buckling

As $350 billion in mortgages hit renewal in 2026, those without the credit scores to refinance at prime rates turned to lenders like GoEasy. This shift is documented in our deep dive into Alternative Financing Trends 2026. In essence, GoEasy acted as a "bridge" for distressed homeowners. The LendCare write-down signals that the "bridge" is beginning to buckle under the weight of record-high Canadian Housing Bubble valuations.

3.2 Credit Metrics: The Hidden Decay

GoEasy’s credit quality had remained stable to moderately improving through early 2025. Key stats: net charge-off (annualized) was ~8.9% in Q1, 8.8% in Q2, 8.9% in Q3 – in line or slightly below guidance. However, the sudden recalibration implies certain LendCare accounts were much riskier than originally thought. The entire incremental C$178M charge-off in Q4 pushed FY 2025 net charge-offs to ~12.9%, a level that signals systemic stress.

IV. Regulatory Headwinds: The 35% APR Cap and the GoEasy Subprime Risk

A critical factor in GoEasy's 2026 decline is the Federal Criminal Rate Cap, which was lowered to 35% APR in January 2025 by the Government of Canada.

4.1 The Margin Squeeze on Subprime Lending

Pre-2025, GoEasy could price for high default risk by charging 45%+. Capped at 35%, the company had to tighten underwriting and shift to "lower risk" secured loans. The 35% yield proved insufficient to cover the actual default rates of 2026. This regulatory pressure is a key part of the GoEasy subprime warning, as it limits the ability of lenders to absorb shocks from the Housing Market Reset.

V. Macro Picture: Canada's Debt-Service Wall and the GoEasy Crash

The Canadian consumer entered 2026 with a household debt-to-disposable income ratio of 180% according to Statistics Canada.

5.1 The 'Renewal Shock' and GoEasy's Exposure

To understand why the credit wall broke, look at a typical household facing the GoEasy subprime warning dynamics:

- Original Mortgage: $1,850/mo.

- 2026 Renewal: $3,100/mo.

- The Delta: -$1,250/mo.

- The Solution: A $15,000 "secured loan" from easyfinancial at 24% APR.

- The Problem: The interest makes the total shortfall $1,550/mo. Within 6 months, the borrower defaults.

5.2 Unemployment and the Subprime Tipping Point

The labor market has softened: RBC Economics expects unemployment to peak ~7.1% in late 2025. Any uptick in joblessness strains non-prime borrowers first. GoEasy’s situation highlights how a specialized lender can be caught in broader economic “bubble” dynamics: when housing or consumer credit situations change, it can impact subprime segments severely.

VI. Timeline of the Collapse: A Path to the GoEasy Subprime Warning

- Aug 6, 2025: Q2 2025 earnings show record loan portfolio of $5.10B (+23% YoY).

- Sep 24, 2025: Short-seller report (Jehoshaphat) alleges fraud and credit issues; GoEasy denies it.

- Dec 2, 2025: CEO change announced: Dan Rees to step down; Patrick Ens named successor.

- Mar 10, 2026: Pre-Q4 update: ~C$178M incremental charge-off (LendCare). GoEasy stock crashes 57%.

VII. Scenario Analysis: The Future of Subprime Credit in Canada

7.1 Case A: The "Controlled Deleveraging"

The extra charge-offs mostly clear out bad LendCare loans, and performance stabilizes. 2026 sees elevated losses but a return to ~9–10% net charge-offs by late 2027. This depends on a "Soft Landing" for the broader Canadian Housing Market.

7.2 Case B: The "Subprime Domino Effect"

The identified charge-offs are the tip of the iceberg. Other segments (secured, unsecured) begin showing higher delinquencies as unemployment worsens. This could lead to a systemic freeze in alternative credit, accelerating the Housing Bubble Collapse.

IX. The Systemic Risk: Alternative Lender Contagion

Here's the thing: GoEasy is high-profile, but it is the tip of a much larger "Alternative Lending" iceberg. In 2026, approximately 12% of the Canadian mortgage market is held by non-prime lenders, including MICs and private debt funds.

So here's what happened: The 57% crash in GSY has triggered a "Risk Re-Rating" across the entire alternative sector.

- Funding Squeeze: Private debt funds are seeing "Redemption Requests" spike as institutional investors move toward the safety of government bonds.

- Margin Calls: Lenders who borrowed against their loan books to expand in 2022 are now facing margin calls as the value (and liquidity) of those subprime loans evaporates.

X. The 2026 Federal Rate Cap: A Regulatory Choke Point

But here's the problem: The timing of the GoEasy subprime warning coincides with a permanent structural change in Canadian lending law.

Here's how it works: The decision to lower the Criminal Rate of Interest to 35% APR (formerly 47%) has removed the "Risk Premium" that allowed GoEasy to survive previous downturns. Without the ability to charge 45% for ultra-high-risk loans, GoEasy is forced to either:

- De-Market: Stop lending to the 2 million "highest risk" Canadians.

- Absorb Losses: Accept that their Net Promoter Score and Profitability will be permanently lower.

Action: For investors and homeowners alike, this means Credit Scarcity is the new reality of 2026. The "Bridge Loan" that saved you in 2022 no longer exists.

VIII. Conclusion: Watching the Canary in the Subprime Coal Mine

On BubbleWatch.ca, we believe the GoEasy subprime warning of March 2026 is the final warning for the Canadian housing bubble. It shows that high-interest debt can no longer be "inflated away" or "equitied away" via rising home prices. When the subprime lenders fail, the prime lenders are next.

This episode is a clear signal to monitor secondary credit markets, not just headline real estate prices. The "debt-service wall" is no longer a theoretical risk; it is a documented reality.

Sources: TSX GSY Profile, OSFI Lending Guidelines, Bank of Canada Monetary Policy, StatCan Debt Data, RBC Economics, Jehoshaphat Research, BubbleWatch Financial Risk Matrix 2026.

Keywords: GoEasy Subprime Warning, GSY Stock Crash 2026, Alternative Lending Canada Risk, 35% APR Cap Impact, Subprime Mortgage Defaults, GTA Condo Credit Crunch, Shadow Banking Crisis 2026, Canadian Household Debt-Service Wall.

Detailed Analysis of GoEasy Ltd. (TSX: GSY) Business Segments

To fully grasp the magnitude of the GoEasy subprime warning, one must look deeper into the three core brands: easyfinancial, easyhome, and LendCare.

1. easyfinancial: The Primary Lending Engine

This is the company’s primary lending arm, offering unsecured and secured consumer installment loans via ~400 branch stores and online channels. easyfinancial originated ~$946 million in loans in Q3 2025 (up 13% YoY). This segment contributed roughly 90% of GoEasy’s total revenue and held ~91% of the loan portfolio. The shift toward secured/home-equity business was intended to diversify risk, but the 2026 housing downturn has turned this "safety net" into a potential liability.

2. easyhome: The Rent-to-Own Legacy

A rent-to-own retail business (furniture, appliances, electronics) with credit underwriting on lease-purchases. This segment is much smaller, with C$150.8M in loan receivables. While its financing rates are high (often exceeding 50% equivalent APY), its scale is less than 3% of GoEasy's book, making it a negligible factor in the GoEasy stock crash.

3. LendCare: The Fatal Growth Engine

Acquired for ~$320M, LendCare is a merchant-finance arm specializing in auto and powersports financing at the point of sale. These loans are typically bigger tickets and purchased through car dealers and powersports retailers. The Mar 2026 charge-off of ~C$178M was entirely LendCare portfolio. Our analysis flags LendCare as the primary vulnerability that triggered the GoEasy subprime warning.

Funding and Liquidity: The Breaking Covenants

GoEasy’s funding structure combines securitization lines, a syndicated revolving facility, and public debt. As of late 2025, it had a $1.4 billion securitization warehouse facility. The upcoming charge-offs will breach covenants on these secured lines. While GoEasy has obtained accommodations (waivers) from its syndicate, the long-term viability of this funding model is in question if losses continue to mount.

The GoEasy subprime warning is not just about one company; it is about the accessibility of credit for Canada’s 10–12 million non-prime consumers. If GoEasy is forced to further tighten its belt, millions of Canadians will find themselves without a safety net, potentially leading to a wave of forced sales in the GTA and GVA markets.

The Regulatory Overhang: 2025 APR Caps and the GoEasy Subprime Warning

The federal government capped the maximum APR on loans under $5,000 at 35% in January 2025. Many of GoEasy’s installment loans previously exceeded this cap, reaching as high as 47.9%. This "regulatory overhang" has compressed yields and forced the company to take on higher-risk, larger loans to maintain margins. The 2026 crash is a direct consequence of this shift, further validating the GoEasy subprime warning.

Legal and provincial risks also persist. For instance, Ontario’s payday-loan regime limits cost of borrowing to $14 per $100. While GoEasy’s product lines largely operate as installment loans outside payday rules, any new provincial legislation or enforcement could constrain product design or margins. The Mar 2026 event highlights how fragile these high-yield models are when regulatory gates close.

Management Transitions Amid the GoEasy Stock Crash

Several leadership moves occurred in late 2025, adding to the uncertainty surrounding the GoEasy subprime warning:

- CFO Turnover: On Sep 16, 2025, GoEasy announced CFO Hal Khouri would leave. Felix Wu, formerly of fintech KOHO, was named Interim CFO. This transition happened just as short-seller reports began to gain traction.

- CEO Succession: On Dec 2, 2025, founder-CEO Dan Rees stepped down due to health concerns. Patrick Ens, who had been President of easyfinancial, took the helm. While the market initially viewed this as a smooth transition, the Mar 2026 charge-off has put Ens under immediate fire.

In response to the 57% stock plunge, management has detailed a 6-point action plan: refocusing growth on easyfinancial's home-equity lending, cutting back LendCare originations, unifying internal operations, finding $30M in annual cost savings, strengthening LendCare leadership, and halting all share repurchases and dividends.

Historical Perspective: The Record-Breaking Quarters of 2025

To understand the shock of the GoEasy subprime warning, one must recall the optimism of 2025:

- Q1 2025: Revenue C$392M (+10% YoY), net income $39.4M.

- Q2 2025: Revenue C$418M (+11%), net income $86.5M.

- Q3 2025: Revenue C$440M (+15%), loan receivables hit all-time high of $5.44B.

For 95 consecutive quarters, GoEasy was a profit machine. The sudden C$178M write-down in Q4 2025 has essentially wiped out the gains of the first three quarters, a reversal that has shaken the foundations of the Canadian subprime lending market.

Regional Divergence: Why the GoEasy Subprime Warning Hits Ontario Hardest

While the GoEasy stock crash is a national event, its impact is far from uniform. TransUnion reports that delinquency trends vary significantly by region. For example, Alberta saw 90+ day delinquencies rise to 2.29%, reflecting continued energy-sector volatility. However, the real concern for BubbleWatch.ca is Ontario.

In the Greater Toronto Area (GTA), the concentration of high-leverage "investor" condos has created a unique vulnerability. Many of these investors used Alternative Financing Trends 2026 to manage negative cash flow. As GoEasy and other subprime lenders pull back, the GTA condo market loses a critical layer of liduidity, potentially accelerating the GTA Housing Reset 2026.

The Shadow Banking Nexus: Beyond GoEasy

The GoEasy subprime warning is a window into the much larger world of Canadian shadow banking. Private lenders, who often charge 10-15% interest, have become the "lenders of last resort" for Canadians failing the B-20 stress test.

GoEasy's LendCare division operated at the intersection of consumer credit and asset-backed lending. When these subprime "bridges" fail, the ripple effect reaches mortgage investment corporations (MICs) and private debt funds. We are beginning to see a "credit crunch" in the non-prime space, which historically precedes a broader correction in prime mortgage markets.

The Short-Seller Perspective: Jehoshaphat Research vs. GoEasy

In September 2025, Jehoshaphat Research released a scathing report alleging that GoEasy's credit metrics were "heavily manipulated" and that the real default rates were being masked by aggressive loan modifications. GoEasy vigorously denied these claims, stating that their $400M loan-loss reserve was more than sufficient. The 57% stock plunge in March 2026 suggests that the short-sellers may have been closer to the truth than management's rosy projections implied.

The Psychology of the 2026 Subprime Borrower

In a high-inflation environment, the subprime borrower is under unique psychological stress. Unlike a prime borrower with three months of emergency savings, a GoEasy customer is often living paycheck to paycheck. When the GoEasy subprime warning signals a tightening of credit, the "credit path" for these individuals vanishes. This leads to "desperation selling" of assets—cars, motorcycles, and eventually, the family home.

Technical Credit Quality Developments and the GoEasy Crash

The sudden recalibration implies certain LendCare accounts were much riskier than originally thought. GoEasy said it has “exhausted all available efforts” to recover some delinquent LendCare loans. The Feb–Mar 2026 update suggests that forward-looking credit models were insufficient – a risk flagged by short-sellers months in advance. This lack of transparency is what ultimately led to the catastrophic GoEasy stock crash.

The 'Wealth Effect' Reversal and the Housing Connection

For years, rising home prices provided a psychological buffer for subprime borrowers. Even if they couldn't afford their monthly payments, they felt "house rich." As the Canadian Housing Bubble begins to deflate, this buffer has vanished. The GoEasy subprime warning is the first major sign of the "wealth effect" reversing, as consumers realize their equity is a mirage.

Investment Implications and the Road Ahead for GoEasy Stock

GoEasy’s share-price collapse reflects a dramatic shift in investor perception: from a “high-growth, high-return” story to a “stressed credit” story. For investors, the key questions are whether GoEasy can exit this crisis in the same powerful growth trajectory, or whether it will languish under heavier losses and low multiples.

If one believes the Canadian consumer and housing market will stabilize and GoEasy’s management executes its turnaround plan effectively, then GoEasy might represent a contrarian opportunity. However, if the macro environment continues to deteriorate, the GoEasy subprime warning may just be the first chapter in a much longer story of financial distress.

Valuation: Is the 57% Drop a Buying Opportunity?

Prior to the crash, GSY traded at 20-25x earnings. Today, it sits at around 5x trailing earnings—but those earnings are "pre-wash." If 2026 remains a year of write-downs, the stock may still be overvalued. The market is effectively pricing in a significant probability of further credit contagion.

Key Takeaways from the GoEasy Subprime Warning

- Credit as a Leading Indicator: The 57% collapse of GoEasy is a "canary in the coal mine" for the broader Canadian economy. It suggests that the household debt stress has moved from "struggling" to "defaulting."

- The Renewal Cliff is Real: The spike in LendCare write-downs confirms that borrowers are sacrificing non-essential debt to protect their homes, a trend that will intensify as $350B in mortgages renew in 2026.

- Regulatory Squeeze: The 35% APR cap has fundamentally altered the risk-reward profile for subprime lenders, potentially leading to a permanent contraction in credit availability for non-prime Canadians.

- Asset Value Sensitivity: As subprime lenders pull back, the "floor" for asset values (cars, motorcycles, and condos) is falling, which may lead to a faster-than-expected deflation of the Canadian housing bubble.

- Funding Fragility: The breach of covenants following a single quarter of losses reveals how thinly capitalized the alternative lending sector remains, exposing systemic risks for the Mortgage Renewal Cliff 2026.

As we continue to monitor the Spring Market Outlook 2026, the GoEasy subprime warning remains the most critical data point for anyone trying to time the bottom of the Canadian housing market.